Unlock Forklift Tax Deductions! Find out how investing in your own equipment can lower expenses!

Forklift Tax Deductions: Buying Equipment Can Put Money in Your Pocket

Purchasing heavy equipment is a significant financial commitment for any warehouse, distribution center, or construction company, but under the current IRS regulations, that investment can be very rewarding for your bottom line. At first glance, the complex world of business taxation can seem daunting, but if you understand how to leverage the tax codes, what seems like an expensive capital expenditure can be a savvy financial move. Thus, it is mandatory to understand the forklift tax deductions before forklift purchase.

One of the most powerful tools available to business owners today revolves around heavy equipment write-offs, designed specifically to stimulate economic growth and allow companies to reinvest in their own infrastructure. If you’re thinking about upgrading your fleet or replacing aging equipment, it’s absolutely critical that you understand the full range of forklift tax deductions.

American Forklifts (americanforklifts.org) is committed to assisting companies in acquiring the most dependable and productive material handling equipment on the market and reaping the financial rewards of their purchase.

Companies can dramatically reduce the upfront cost of new or used equipment using tools like Section 179 and bonus depreciation. This comprehensive guide will walk you through everything you need to know about navigating these incentives, so that you keep more of your hard earned capital within your operations where it belongs.

Forklift Tax Deductions and Section 179: What You Should Know in 2026

Business owners are often skeptical when they hear the term “tax break” about how much they will actually benefit. But the Section 179 deduction is not some arcane loophole. It is a straightforward, purposeful incentive created by the government to encourage small and medium-sized businesses to invest in themselves by purchasing necessary equipment.

Under normal circumstances, when a business buys a large asset such as a forklift, they must capitalize the cost and depreciate it over a number of years. That means a $50,000 forklift may only allow a $10,000 deduction per year for five years. That’s better than nothing, but it doesn’t provide the immediate financial relief that many growing companies need to manage cash flow effectively.

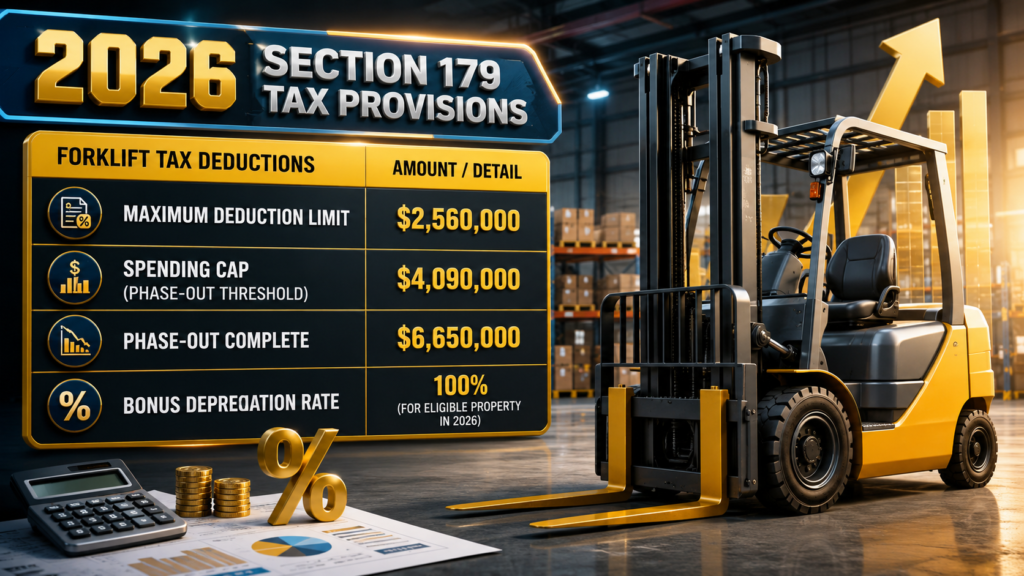

Section 179, however, reverses this dynamic by permitting businesses to deduct the full purchase price of qualifying equipment from their gross income in the same year that the equipment is placed into service. The IRS has established some very favorable limits for the 2026 tax year with a max deduction of $2,560,000 on qualifying equipment.

This means that whether you are buying a single reach truck or outfitting an entire massive warehouse with a fleet of heavy-duty pneumatic forklifts, the initial financial sting is drastically reduced by your tax savings.

Table: Forklift Tax Deductions

| 2026 Section 179 Tax Provisions | Amount / Detail |

| Maximum Deduction Limit | $2,560,000 |

| Spending Cap (Phase-out Threshold) | $4,090,000 |

| Phase-out Complete | $6,650,000 |

| Bonus Depreciation Rate | 100% (for eligible property in 2026) |

Here’s the important stuff to know about these standard limits:

- Section 179 enables business owners to deduct the full purchase price of equipment in the year of purchase, instead of waiting years to get the cost of the equipment back through depreciation, thereby keeping critical working capital available for other immediate operational needs.

- The primary objective of this specific tax code is to promote business growth by offering significant incentives for the modernization of material handling fleets and general commercial infrastructure.

- Forklifts make the perfect candidate for this tax break because material handling equipment is considered to be essential business equipment and is recognized by the IRS as qualifying property.

Eligibility Requirements: Is your Forklift purchase eligible?

The internal revenue service has laid down a specific set of rules for getting forklift tax deductions, but the good news is that these rules are pretty simple for the average commercial business.

The most basic requirement is that the equipment must be purchased and placed in service between January 1 and December 31 of the tax year for which you’re claiming the deduction. “Placed into service” is a very specific legal term of art; paying for the forklift isn’t enough to qualify.

The equipment has to be delivered, put into operation and ready to go in your facility for its intended use before the clock strikes midnight on New Year’s Eve. The IRS also requires that the equipment be used primarily for business. In tax speak, “primarily” means that the forklift must be used for your trade or business more than 50% of the time. If you use the asset 100% for your business, you can claim the full purchase price.

But if you are in a situation where the equipment is used 80% of the time for business activities and 20% of the time for personal hobbies, your deduction will only be for the 80% business use portion.

Finally, your total Section 179 deduction cannot exceed your net taxable income from the business for the year; you cannot use this deduction in particular to run at a net loss, though generally any unused amounts can be carried forward.

Check that you meet the following baseline criteria before you make your final purchase:

- The equipment must be used for legitimate business operations and for income-producing activities more than 50% of the time to qualify for any level of deduction.

- The forklift must be delivered and placed in operational service by December 31 of the applicable tax year in order to qualify for the filing for that particular year.

- Both brand new models and used forklifts (as long as they are newly purchased by your particular business entity) are fully qualified for these lucrative tax advantages.

Second hand forklifts or new? Which one gets the most tax relief?

One of the more commonly misunderstood aspects of forklift tax deductions is the notion that only brand new, straight from the factory equipment qualifies for government incentives.

This is absolutely false, lucky for the penny-pinching fleet managers. Section 179 regulations treat new and used equipment the same as long as the machinery is “new to you”. In other words, you cannot buy a forklift from yourself, a related party or an entity you control and claim the deduction but you most definitely can buy a refurbished or certified pre-owned lift truck from American Forklifts and get the same percentage of tax relief as if you bought the latest model.

This flexibility is highly strategic for businesses looking to leverage their buying power. As a used forklift is already priced with a lower initial price tag due to normal market depreciation. The net cost of acquiring heavy machinery drops to a remarkably low figure when you add in the lower sticker price and the 100% tax write-off in the first year of ownership.

This enables small and mid-sized businesses to either increase their operational capacity, add redundant backup machines to avoid downtime, or upgrade altogether without debilitating corporate debt. Savvy operators routinely outpace their competitors in asset management by looking at used equipment through the lens of Section 179.

Choose your equipment type using these strategic advantages:

- Section 179 rules work just as well for used forklifts as for brand new ones, meaning you can take advantage of huge tax write-offs for discounted machinery.

- Reliable used equipment extends your capital expenditure budget significantly further, giving you a higher return on investment per unit.

- Buying used assets enables you to avoid the heavy depreciation of new models upfront and still maximize your tax benefit within the legal limits.

How Bonus Depreciation Can Help Your Savings Plan

While Section 179 is usually the first tool business owners reach for to reduce their tax liability, it is not the only mechanism for forklift tax deductions. Bonus depreciation is a great secondary layer of financial relief especially for larger organizations that may exceed the standard Section179 spending caps. For the 2026 tax year, bonus depreciation allows businesses to deduct up to 100% of the cost of qualified property in the year it is placed in service.

The interaction of these two codes is very helpful. Typically, businesses will take their Section 179 deduction to fully offset their net taxable income (up to the $2,560,000 limit). Bonus depreciation can help fill in the gap if your company bought more equipment than the Section 179 limit allows or your purchases exceed your total taxable income.

Bonus depreciation is not as strictly limited to your business’s net income as Section 179 — meaning, technically, you can use it to create a net operating loss that can be carried forward to offset income in profitable years to come. This two-tiered approach is the ultimate tax shelter for heavy industry.

This pretty much ensures that whether you are a small startup purchasing a single pallet jack or a national logistics hub shelling out millions on automated guided vehicles and heavy container handlers the tax code is drafted to subsidize your expansion and reward your capital investments.

As part of your financial planning, consider these bonus depreciation mechanisms:

- Bonus depreciation and Section 179 work together. Bonus depreciation applies if you exceed spending limits or reach net income limits.

- Bonus depreciation can be used to create a net operating loss for your business, providing extreme flexibility, unlike regular Section 179 rules.

- Eligible businesses can take advantage of a bonus depreciation rate up to 100% on qualifying assets in 2026, significantly reducing the effective net cost of large fleet acquisitions.

Buy Outright vs. Finance: How It Affects Your Deductions

One of the biggest misconceptions business owners have is that they need to drain their cash reserves and buy equipment outright to qualify for strong forklift tax deductions. In actual fact, the U.S. tax code is much more generous. You can definitely finance your equipment (or use certain types of leases) and still get the maximum Section 179 deduction.

This strategy is commonly referred to as “Section 179 Qualified Financing” and is one of the best ways to maintain a healthy flow of cash while aggressively reducing tax liabilities. If you finance a forklift, you are still the owner of the equipment for tax purposes.

Therefore, you can deduct the full purchase price of the machinery in the current tax year, even though you have paid only a small fraction of that total price in the form of a down payment and a few monthly installments.

In many profitable situations the cash saved from the immediate tax deduction will be much larger than the sum of the loan payments made in that first year. In short, the government tax savings pays for your cost of financing, and allows the equipment to turn a profit for your business long before you pay it off. However, not all leases qualify for the write off.

Generally, capital leases do, and true operating leases (where you basically just rent the equipment and give it back) do not.

Think about the financial dynamics of how you’ll pay for the equipment you need:

- You can take the whole Section 179 tax deduction right away, even if you finance the forklift through a traditional lender or a qualified capital lease agreement.

- You can deduct the entire cost of the equipment on your tax returns which greatly enhances cash flow while only paying a small percentage of the cost in initial loan payments.

- Operating leases usually don’t qualify for these specific ownership-based deductions so you must carefully structure your financing agreement to qualify.

How to Claim Your Forklift Tax Savings A Step-By-Step Guide

But to benefit from forklift tax deductions, it’s not just a matter of making a purchase, it takes meticulous documentation and precise execution during tax season. Your own bookkeeping needs to be perfect because the IRS is very careful to make sure the right large equipment deduction is made.

It all starts the second you choose to buy from American Forklifts. You are to obtain and keep all physical and electronic documentation including purchase orders, binding contracts, financing agreements and most importantly, delivery receipts that clearly show the machinery was delivered and operational before the end of the tax year.

Now that you have your documentation collected, you need to figure out the exact percentage of business use. If your equipment is used only at your commercial facility then this is an easy 100%. If mixed use you need to maintain a good log to justify your prorated percentage.

The final step in claiming the deduction is to actually do it on IRS Form 4562 and attach it to your regular business tax return (corporate or personal). Every year, tax codes change slightly and there are phase-out thresholds that can be confusing. It is best not to try and figure this out without a professional.

The best way to make sure that you are capturing every single dollar that you are legally owed while staying perfectly compliant with federal law is to partner with a Certified Public Accountant (CPA) who specializes in commercial depreciation and equipment write-offs.

Table: Forklift Tax Deductions Process

| Step in the Process | Action Required by Business Owner | Corresponding IRS Documentation |

| 1. Eligibility Check | Confirm equipment meets >50% business use rule. | Internal Usage Logs |

| 2. Finalize Acquisition | Purchase, finance, and place into active service by Dec 31. | Invoices & Delivery Receipts |

| 3. Calculate Deduction | Prorate total cost based on the exact business use percentage. | Internal Accounting Records |

| 4. Execute Tax Filing | Submit the proper depreciation and amortization paperwork. | IRS Form 4562 |

Follow these protocols you are required to use to protect your write-offs:

- Keep meticulous, organized records of all purchase invoices, manifests, delivery dates, and daily usage logs so you can easily survive any potential IRS audits.

- Complete and attach IRS Form 4562 to your annual tax returns to formally claim and receive your Section 179 and bonus depreciation deductions.

- Always work with a certified tax professional or CPA to double-check your specific numbers and make sure your corporate filing is spot on with current federal rules.

FAQs: Forklift Tax Deductions

Can you write off a forklift under Section 179?

Yes, absolutely. The IRS classifies forklifts and other material handling equipment as “business equipment” and tangible personal property. This makes them an ideal, common candidate for the Section 179 tax deduction, allowing you to deduct the purchase price from your gross income in the year they are put into service.

Can used forklifts be used for Section 179?

“Yes. Section 179 tax deductions are available for used and new equipment. The one thing the IRS is strict on is that the equipment be “new to you” or your specific business entity. You can’t just buy a machine from a related party or a sister company to get a new tax write-off.

The maximum Section 179 deduction for 2026 is $1,220,000.

The limit on the Section 179 deduction is significantly raised to $2,560,000 for the 2026 tax year. Additionally, this huge deduction doesn’t even begin to phase out on a dollar-for-dollar basis until your total business equipment purchases for the year exceed the $4,090,000 cap.

Can I still take Section 179 and finance the forklift?

With a qualified equipment financing arrangement, you can deduct the full Section 179 amount up front. This is very popular as you get the full tax benefit of the total purchase price immediately, although your actual cash outlay for that year is limited to just a few monthly finance payments.

How long do I have to make a claim for forklift tax relief?

To get a deduction in a given tax year the forklift must be bought and fully “placed into service” by December 31 of that same year. But if you buy the machine on December 28, but it doesn’t arrive and is in use until January 2, the deduction gets pushed to the next tax year.

What if a forklift is used for part of business?

The equipment must be used for business more than 50% of the time in order to qualify for a deduction. If you use it 75% of the time for business and 25% of the time for personal purposes, you can only deduct 75% of the purchase price of the forklift using Section 179. To prove this percentage, accurate usage logs must be kept.